Some links in this post are from our partners. If a purchase or signup is made through our partners, we receive compensation for the referral.

Have you invested, or are you thinking about investing in your TFSA? Are you wondering what all the hype is about?

As the TFSA is still relatively new (started in 2009), Canadians aren’t usually as well versed in the tax benefits they offer like they are with the RRSP.

While I won’t give you a full, in depth comparison of these two accounts in this article, there is an important difference between these accounts when it comes to making contributions.

Unlike RRSP contributions, TFSA contributions are not tax deductible and therefore they won’t reduce your taxable income.

Open a TFSA with Wealthsimple Invest Today ($25)

Earn a $25 Bonus with Sign – Up

- Tax-Free investment income

- No account minimum

- 100% free to sign-up

- Wealthsimple is designed for beginner investors

- Wealthsimple invests your money for you

For example, if your earned income for the year is $50,000, a $5,000 TFSA contribution will not reduce your taxable income to $45,000.

In contrast, if you contributed that $5,000 into your RRSP instead, you would be reducing your taxable income by the $5,000 contribution amount – assuming you claimed your entire contribution.

A lot of questions in the world of personal finance can have very wishy washy answers. You’ll hear a lot of “it depends” in the answer, but not for this question.

TFSA contributions will not reduce your taxable income, end of story.

With all of this said, you might be now wondering, well what’s the point of contributing to a TFSA if my contributions aren’t tax deductible, why not just contribute to my RRSP?

Simply put, TFSAs also offer great tax advantages that shouldn’t be ignored. Keep reading.

Open up a TFSA with Wealthsimple Invest Today and Earn a $25 Sign Up Bonus.

Why You Should Still Invest in Your TFSA

If you’re feeling a little bummed out now that you know TFSA contributions aren’t tax deductible, I don’t blame you, I was too.

I cried for 3 days.

Despite this fact though, there are still a lot of reasons why you should invest in your TFSA. Here are a few of those reasons.

Investments Grow Tax Free

Similar to an RRSP, any investment returns generated within your TFSA will typically grow at a tax-free rate.

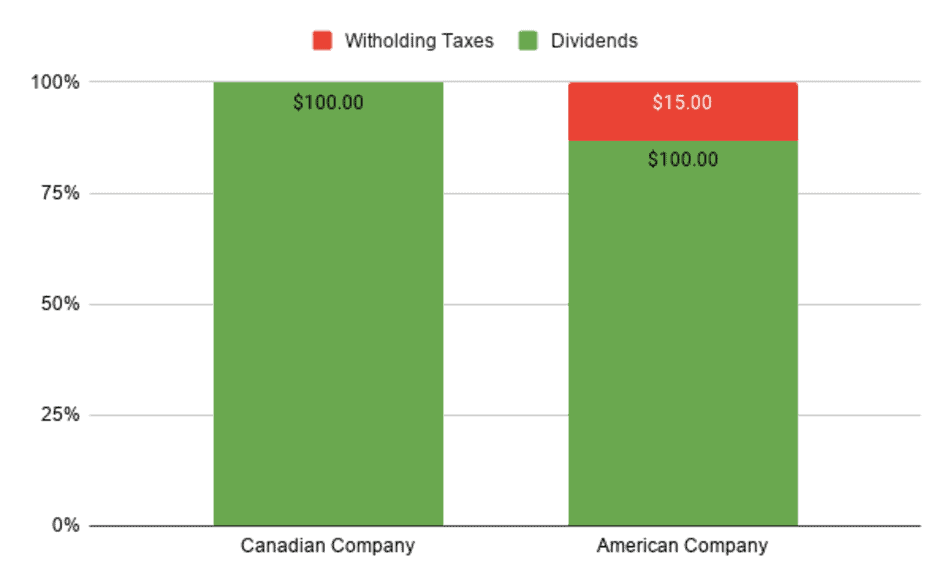

For example, if you hold a Canadian stock (Dollarama, for example) that pays you $100 in dividends for the year, you will not be taxed on this $100 return when you receive the payment or when you withdraw it from your TFSA.

However, it is important to note that dividends paid to Canaidan investors from American companies are subject to a 15% foreign withholding tax – even if these investments are held within a TFSA.

Withdrawals Are Not Taxed

Unlike your RRSP, any withdrawals you make from your TFSA will not be taxed.

As mentioned in my above example, if you decided to withdraw your $100 dividend earnings from your TFSA, you wouldn’t be required to pay any form of taxes on that withdrawal.

If you wanted to withdraw dividends you earned from an American company (Apple, for example), you still wouldn’t be taxed on your withdrawal, however, before the dividends even entered your TFSA, they would have been reduced by 15%.

For example, if you earned a $100 in dividends from Apple, you would only receive 85% ($85) of those earnings due to withholding taxes.

If you decided to withdraw that $85, it doesn’t matter where it came from, you won’t be taxed on the withdrawal.

For a more in depth answer on TFSA withdrawals and how they aren’t taxed, check out this article by The Financial Geek.

Flexible Withdrawals

TFSA withdrawals are amazing. Bold statement I know, but hear me out.

The withdrawal rules associated with most registered investment accounts are usually confusing and quite overwhelming. But there really aren’t any rules when it comes to withdrawing money from your TFSA.

You can withdraw as much money as you wish, tax-free!

Not only that, but you can make as many withdrawals as needed, again, tax free!

Take that RRSP! My gosh, the CRA essentially takes your soul away for any RRSP withdrawals. Not for the TFSA though, as long as you have money to withdraw, take out as much as you want, as many times as you want!

Quick Note #1 – It is possible that the financial institution that issues your TFSA could charge you a fee for making withdrawals, so make sure you check this beforehand.

TFSA Withdrawals Won’t Impact Your Contribution Room

Even though TFSA contributions aren’t tax deductible, they offer other great advantages that certainly make investing in them worthwhile.

But wait, there’s more!

Similar to an RRSP, TFSAs have set contribution limits each year that you shouldn’t exceed – unless you enjoy paying tax penalties!

But the great thing about TFSA withdrawals is that you’re able to re-contribute what you withdrew in the following year.

In other words, whatever the dollar amount is that you withdrew for the year, that amount will be added to your contribution room for the following year.

Quick Note #2 – Your TFSA contribution room will reset every year on January 1st .

Quick Note #3 – Make sure you don’t overcontribute to your TFSA. While you can replace your TFSA withdrawals in the same year you made them, you can only do so if you have contribution room available. If you’ve already maxed out your contributions, your additional contribution room won’t be added back until January 1st of the following year.

Hopefully by now I’ve been able to convince you to invest in your TFSA despite the obvious drawback of not being able to deduct your contributions from your income.

But don’t go crazy now! Even though TFSAs are sweet financial vehicles, there’s a limit to how much you can contribute.

How Much Can You Contribute to Your TFSA?

The amount you can contribute to your TFSA depends on a few factors, so it really depends.

Simply put though, your total contribution room depends on your age and the total amount you’ve already contributed.

As time goes on, the amount you are able to contribute to your TFSA will grow as the CRA adds additional contribution room to your account each year.

Here is a chart that illustrates these annual TFSA contribution limits.

| Year | TFSA Limit |

|---|---|

| 2020 | $6,000 |

| 2019 | $6,000 |

| 2018 | $5,500 |

| 2017 | $5,500 |

| 2016 | $5,500 |

| 2015 | $10,000 |

| 2014 | $5,500 |

| 2013 | $5,500 |

| 2012 | $5,000 |

| 2011 | $5,000 |

| 2010 | $5,000 |

| 2009 | $5,000 |

Quick Note #4 – Remember that you won’t lose any contribution room by making TFSA withdrawals.

I know this stuff can be overwhelming, so if you are a little confused and just want to know what your current TFSA contributions room is, just follow this simple 5 step process below and forget everything else.

How Can I Check My TFSA Contribution Room?

Step 1 – If you haven’t already, register your online CRA account.

Step 2 – Sign in to your CRA account.

Step 3 – Scroll down to the bottom of the homepage until you see “TFSA Contribution Room”.

Step 4 – Subtract any contributions made in the current year from your TFSA contribution room.

Step 5 – The number you get is your current TFSA contribution room.

For more information on how to check your contribution room and other information on TFSA contributions, check out The Financial Geek’s article How Can You Check Your TFSA Limit?

Conclusion

So let’s finish this article by restating the answer to the main question here.

I can’t make it any more clear than this – TFSA contributions will not reduce your taxable income.

You don’t even have to take my word for it! Here is a screenshot directly from the CRA website stating this fact.

Hopefully this fact doesn’t deter you from investing money in your TFSA all together though. As discussed above, TFSAs have some great tax benefits that you should certainly take advantage of.

But again, don’t go crazy with contributions.

Similarly to your RRSP, there is a limit to how much you can contribute. If you’re not careful, you could accidentally over-contribute and be hit with a tax penalty.

If I’ve taught you anything from this article, I want it to be this, personal finance is a terribly dry subject, how have you read this far?

Allow me to take you out of your misery.

Geek, out.

How to Open a TFSA with Wealthsimple (4-Step Guide)

If you are interested opening up a TFSA for yourself, check out The Financial Geek’s Step-by-Step Guide on how to do so with Wealthsimple.