If you live paycheck to paycheck, investing money can be hard. It often seems impossible.

You always tell yourself that you’ll invest whatever you have left over at the end of the month, but what happens at the end of each month? You have nothing left over! That’s just human nature.

I’ve been there before, and it’s not fun. Work hard, earn money, spend money, repeat. You feel like you’re in a rat race that will never end.

But here’s the thing, investing money while living paycheck to paycheck is quite possible, you just have to learn how to set things up properly, allow me to explain.

Here is a 5-step process in how you can invest money while living paycheck to paycheck.

- Determine the percentage of your income that you’re going to invest.

- Create a new budget with your new investment amount included.

- Open up an investment account.

- Setup automatic deposits from your bank to your investment account.

- Stick to your new budget.

So you might have read those 5 steps and felt a little underwhelmed, it seems quite obvious doesn’t it?

But allow me to talk you through each step so you can see why each step is so important to the entire plan.

| Ready to Invest? | Our Recommendations | Start Investing Today |

|---|---|---|

| Wealthsimple Invest ($25 Bonus)Only in Canada

| Start Investing TodayRead our Review |

BettermentOnly in USA

| Start Investing Today |

1. Determine the percentage of your income that you’re going to invest

Okay, first things first – how much do you think you could realistically invest on a monthly basis?

Now I know what you are thinking, “I can’t afford to invest anything!, that’s why I’m reading this stupid article!”

Okay, fair point. But my argument is that you actually can’t afford not to be investing and saving for retirement.

I personally recommend trying to save 10% of your pre-tax income. Now maybe that is too much for you right now, and that’s okay. But invest at least 5% of your income to get the ball rolling.

Don’t think about anything else right now, don’t worry about how you’re going to pay for this or pay for that, we will get to that later, for right now, just commit to saving at least 5% of your income.

As Tony Robbins says, treat this 5% like a tax, no matter what, you have to pay this 5% – but instead of paying it to the government, you are paying it to yourself.

Okay, so that’s basically it for step 1 – pick a percentage of your pre-tax income that you are going to invest. I’d recommend anywhere in the ranges from 5%-15%.

Once you get this done, move on to step 2.

2. Create a new budget with your new investment amount included

Investing while living paycheck to paycheck is not easy, I’m not trying to say that. But it’s certainly achievable if you budget for it correctly.

And listen, your budget doesn’t have to be fancy, I literally use an excel spreadsheet for mine, I will include a picture of it here below.

So as you know can see, I don’t have anything fancy going on here. I won’t go into a full discussion here on how to properly create a budget – but here is the one thing you do need to do.

Budget for your investments before anything else. Obviously taxes will be taken out of your paycheck first, but after that, the first thing you need to account for is your investments.

So if you make $30,000 and you decide to invest 5% of your income, then you need to budget $125/month towards investing.

$125 = ($30,000/12 months) x 5%

Now that you’ve budgeted for your investments, you can now start budgeting for your other expenses based on the amount of free cash flow you have left after your taxes are paid and investments have been made.

These other expenses will include things like rent, mortgages, car expenses, entertainment costs, food, binge drinking (wait, what?), gas, childcare expenses, etc.

Here is where you may need to make some cutbacks, but you might realize when making a budget that you don’t even need to make that many cutbacks, you just need to give every dollar you earn a purpose.

I use an app called Mint to help me track where I’m spending money. It is a great app for budgeting.

We often spend our money on things we don’t even care about and that impacts our ability to spend it on things that really matter and will make a difference in our lives – such as an investment fund.

Okay, I’ll stop rambling now. But it’s time to make a budget.

I’ve said it before but I’ll say it again now – you can’t afford not to invest!

Budget for your investments FIRST, and then spend the rest on everything else. Not the other way around, because as we know, money doesn’t last long in our bank accounts.

3. Open up an investment account

Okay, now that you have decided on what percentage of income you are going to invest and you’ve made a budget for it, it’s time to start putting your plan into action.

It’s time to open an investment account. Now this step is pretty forward, and it can be pretty exciting too.

I’d recommend choosing one of these two online financial institutions to start your investing with.

I’ve included links in the “Here’s Why” link above which goes into more detail on why I recommend investing with one of these two financial institutions.

But in short, if you are brand new to investing and want to have more of a hands off experience, I’d recommend Wealthsimple.

If you want a more hands on approach and you want to be able to pick your own stocks and other investments – go with Questrade.

I personally use both platforms to do my investing with, and I have nothing but good things to say about both companies.

They’re safe, reliable and very transparent about everything they do.

Once you set up your account, move onto step 4 – arguably the most important step of them all!

| Ready to Invest? | Our Recommendations | Start Investing Today |

|---|---|---|

| Wealthsimple Invest ($25 Bonus)Only in Canada

| Start Investing TodayRead our Review |

BettermentOnly in USA

| Start Investing Today |

4. Setup automatic deposits from your bank to your investment account

So now moving on to step 4.

As just mentioned, for people looking to invest money while living paycheck to paycheck, this step is vital to the success of your plan.

You need to set up regular deposits that automatically take money out of your bank account and into your investment account.

Most of us, including myself, don’t have the discipline to do it ourselves every month. As stated above, we tend to spend whatever we have in our day to day banking account – it’s just human nature.

I recommend you set up your automatic deposits for the same day(s) you get paid each month.

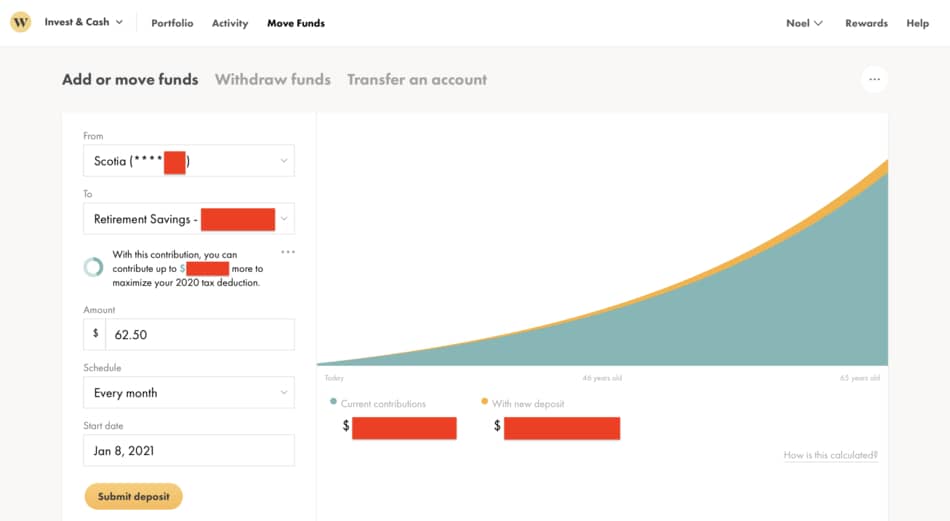

So for example, using the same numbers as above, if you invest $125 a month and you get paid on the 15th and last day of each month, set up your automatic deposits so that $62.50 leaves your bank account and enters your investment account on these payment dates.

This way, you are forcing yourself to save each and every month by taking your investment money off the top of each paycheck you earn.

Now you won’t be tempted to spend money that should be invested because you simply won’t have it in your account. It’ll be gone into your investment account by the time you wake up.

How you go about setting up your automatic deposits really depends on what type of investment firm you deal and who you bank with.

But I can almost guarantee you that this option will be possible with whoever you’re working with.

I mentioned earlier that I use Wealthsimple for some of my investing, below is a screenshot of my actual account and the page where I set up my automatic deposits. As you can see it has a very modern, easy to use interface.

Once you have your investment account open and you’ve successfully set up your account with automatic deposits, you basically have all the upfront work done.

Now it’s time to execute on the plan.

5. Stick to your new budget

The last step in this 5-step process to investing while living paycheck to paycheck is to successfully stick to your budget.

Out of all 5 of these steps, this is probably the hardest of them all.

Why? Because this isn’t something you do once and it’s over, this is something you continually need to act on.

I mentioned Mint before, but I will briefly mention them again here now. Mint is a free app that tracks and categorizes your spending for you. I personally use it as a tool to help ensure I don’t overspend in certain areas (usually entertainment costs for me – guilty!).

Everydollar.com also writes a great article here that talks about a number of different tips and tricks on how people like you and me can stick to a budget.

My top 3 tips would be to avoid credit cards, track and categorize your spending, and avoid large unnecessary purchases.

Conclusion

So here’s the bottom line, investing is very much possible even if you’re living paycheck to paycheck.

The percentage of income you choose to save and invest is not dependent on how much you make, it depends on what you decide to do with the money you do earn.

I know people making $125,000 a year that are far less wealthy than another person making $50,000 a year.

How? Because unlike the high income earner, the $50,000 earner chooses not to spend every cent she earns and invests 10% of her paycheck each and every month.

Here’s the funny thing. While investing a percentage of your income each month means you’ll have less free cash flow to spend on other things – it’ll actually make you happier.

Having peace of mind in knowing that your financial future looks bright is a much better feeling than spending an extra couple dollars each month on who knows what!

Trust me, I’ve been on both sides of this fence, I choose to invest.

And that’s it really! I hope this 5-step process will help those of you living paycheck to paycheck to begin investing.

Remember, it doesn’t have to be a lot, it just has to be something.

Geek, out.

![How to Invest in Canadian Stocks [5 Simple Steps]](https://thefinancialgeek.com/wp-content/uploads/2021/01/How-to-Invest-in-Canadian-Stocks.jpg)

One Comment

Comments are closed.