If you want to retire early as a Canadian, you are not alone.

The average age of death in Canada is roughly 82 years old, that only leaves us with roughly 17 years to live if we retire at the typical age of 65. And there is no guarantee on that either.

Canadians are starting to realize that life is too short to work until their mid 60s and they’re looking for opportunities in which they can retire earlier.

With that, I have compiled a list here of 15 tips and tricks to help Canadians retire earlier than normal.

1. Take Advantage of Your RRSP

If you’re a Canadian, you have the luxury of using certain financial vehicles that others don’t – one being the RRSP.

An RRSP (Registered Retirement Savings Plan) is a financial account that helps Canadians save for retirement in a tax efficient manner.

RRSPs were established by the Canadian Government in the late 1950’s and come with many tax benefits that will speed up any Canadian’s retirement plan.

RRSP Tax Benefits

- Reduces Taxable Income – Depending on your situation, this could mean you get a big tax rebate every year that you can then re-invest into your retirement plan.

- Tax-Deferred Growth on RRSP Investments – You don’t have to pay taxes on capital gains, dividends or interest generated from your investments held within your RRSP until you retire.

I will include an article I wrote here that goes more in depth on RRSPs.

Long story short though, if you don’t open up an RRSP account, I’m not saying you won’t retire early, but you’re putting yourself way (way way way) behind the pack.

I opened up an RRSP with Wealthsimple, I highly recommend them if you don’t already have an RRSP.

For an in-depth review, here is my recommendation post on Wealthsimple.

Open up a RRSP with Wealthsimple Invest Today ($25)

Earn a $25 Bonus with Sign – Up

- RRSP contributions are tax deductible

- Very simple sign-up process

- No account minimum

- Account creation is 100% free

- Modern user interface

2. Start Investing as Early as Possible

As Canadians, financial literacy is something that we were never really taught in school.

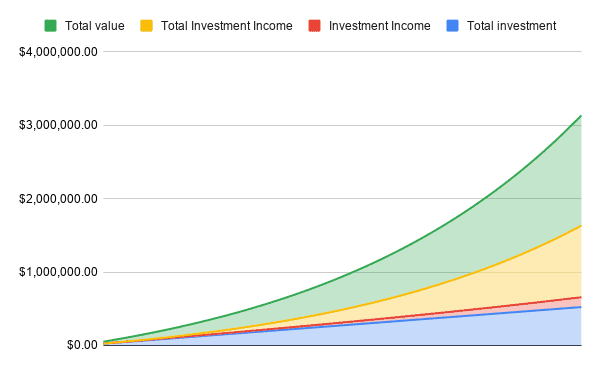

Which really sucks, because if someone told us that investing $300 a month from ages 20 – 55 would leave us with $1,138,991.42, then I’m sure more Canadians would start investing at an early age.

I can’t stress enough how important it is to start investing as early as possible if you want to retire early in Canada.

If you’re wondering where those numbers came from above, I just used this compound interest tool and used a 10% average return – the math checks out!

Those that don’t start investing early have a much lesser chance of retiring early than someone who does. Check out this scenario below.

Nicole starts investing at age 35, she invests $500 a month from 35-55. During those 20 years, she generates an average return of 10%.

Total Contribution: (12 months x $500 month) x 20 Years = $120,000

Average Return on Investment : 10%

Total Value of Investment at 55: $379,684.42

Sarah on the other hand, starts investing at age 25 but invests only $300 a month from ages 25-55. She also generates an average return of 10% over the 30-year period.

Total Contribution: (12 months x $300 month) x 30 Years = $108,000

Average Return on Investment : 10%

Total Value of Investment at 55: $678,146.38

So as you can see, Sarah actually invested $12,000 less than Nicole, but ended up with roughly $300,000 more than her at age 55.

How?

Because when you start investing at a young age, you get the compound interest snowball effect working early, and once it gets going it is a very powerful force.

Think about it, Sarah invested less money but ended up with $300,000 more at age 55.

Open up a RRSP with Wealthsimple Invest Today ($25)

Earn a $25 Bonus with Sign – Up

- RRSP contributions are tax deductible

- Very simple sign-up process

- No account minimum

- Account creation is 100% free

- Modern user interface

3. Create Other Income Sources

As Canadians, we are lucky to be born into such a great country with a strong economy.

And while having a job is great, consider creating other income sources that you can rely on outside of your job.

I heard the saying before that job just stands for Just Over Broke. While I don’t think that’s always the case, I do think it has some merit.

By diversifying your income streams, you’ll not only be able to save and invest more money for retirement, but you may also be able to rely on these streams of income during retirement.

Now I’ve previously written many articles on how people can make money outside of a job, so I’ll include a few of those links below.

- Make Money Online as a Beginner | 17 Proven Ways

- 9 Easy Ways to Make Money Without Owning a Business

- Make Money on a Website Without Selling Anything | 7 Simple Ways

- 9 Legit Ways You Can Make $1,500 a Month From Home

- 13 Proven Ways to Make Money When You Don’t Have Any Money

While there is likely some overlap in these articles, I would definitely recommend reading through one or two of them for some side-hustle inspiration.

One way I’ve been able to successfully create another source of income for myself is through blogging. While it takes a bit of time to build a following, it’s a very rewarding experience and something I’ve enjoyed doing that’s made me more money then I thought it would.

For a step by step guide on how to start a blog, check out my article Start a Blog in 3 Easy Steps | Step by Step Guide (2022) This article will give you a detailed, step by step guide on how to about getting a blog setup. It’s the exact same method I use for setting up the current blog you are reading, and again – it’s really inexpensive. The web-hosting platform I recommend is less than $5 per month.

How to Start a Blog in 40 Minutes | The Financial Geek’s 3-Step Guide (With Screenshots)

4. Set a Financial Goal and Track Your Progress

I am a strong believer in setting financial goals.

If your goal is to retire early, that’s great, mine too, so figure out the amount you’ll need to retire comfortably on and then work backwards from there.

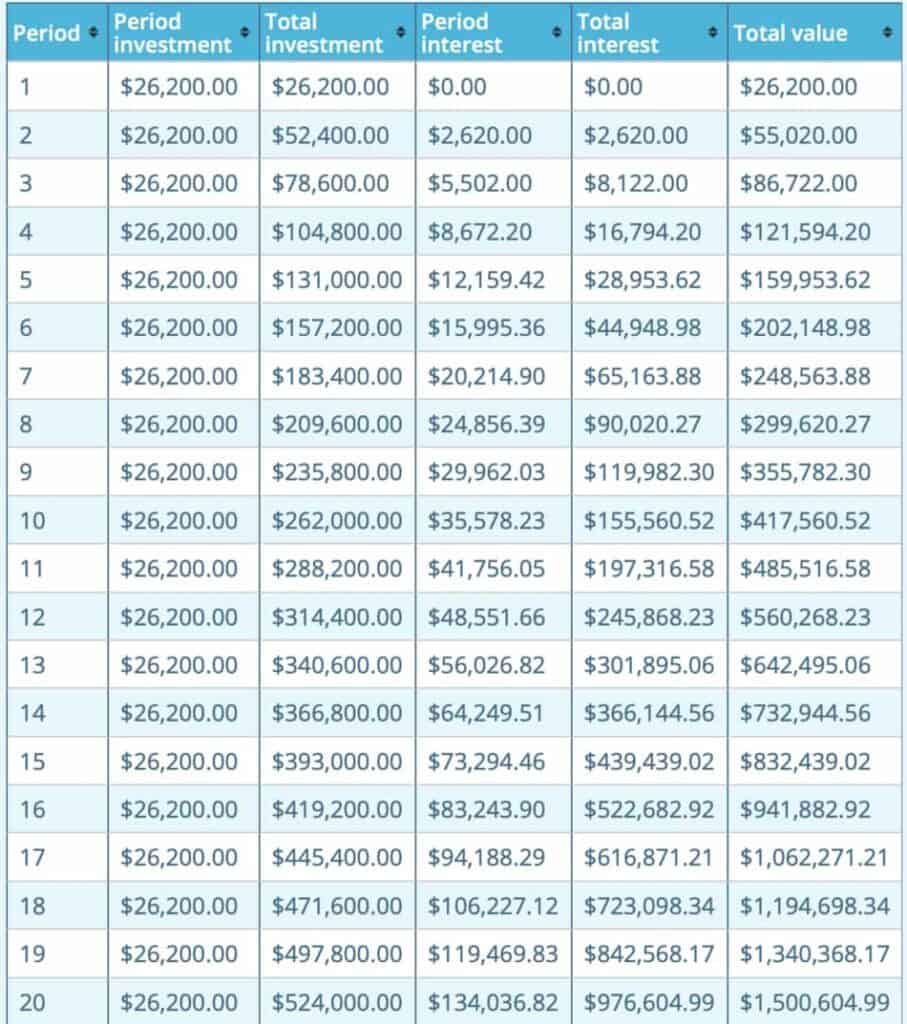

For example, let’s say you want to retire in 20 years with $1,500,000.

How much will you need to save and invest each year to hit that target? Assuming you have nothing in your retirement savings now, you’ll need to invest roughly $2,183 per month ($26,200 per year) at a 10% return to retire in 20 years.

Then you need to track your progress every year, are you hitting your annual goals in terms of savings and investment returns?

If not, do you need to save more? Or maybe you need to aim for a higher return by investing differently.

Whatever you have going on, it is so important you create a plan and then stick to it.

Determine how much you want to retire with and then go to the compound interest calculator and figure out how much you’ll need to invest each month and at what return.

Then it’s your job to execute on your plan. Earn, save, invest, returns – on repeat until you retire.

5. Never Finance a Vehicle

I will keep this tip pretty short, but if you want to retire early as a Canadian, never finance a vehicle.

Canadians believe that buying a brand new car and making monthly payments on it is normal.

“It’s just part of life” as they say.

And it’s no surprise we think that, it’s hard to watch anything now without being bombarded with ads on the greatest new vehicles that are on the market. Automobile manufacturers spend big money on getting their prize possessions in front of potential buyers.

Don’t be a potential buyer! And if you are, pay cash!

I’m telling you right now, spending $400-$500 a month on a car payment is not the pathway to early retirement.

Instead save up cash for a used, but reliable, vehicle and invest what “normal” people pay every month in car payments.

Remember, $500 invested over a 20-year period equates to roughly $380,000 dollars (10% ROI).

You know what’s going to happen anyway! After a few weeks of driving in a new car, the novelty wears off and you won’t care what you’re driving.

You know what won’t wear off though, the bank asking you for their money every month.

6. Try and Max Out Your TFSA

Maxing out, or coming close to maxing out your TFSA is a great way to save for early retirement as a Canadian. While a TFSA wasn’t designed specifically for retirement, it can certainly be used for it.

Do you have a TFSA open already? If not, you really want to open one. I recommend opening one with Wealthsimple for the reasons outlined in my article here.

If you’re not familiar with TFSAs, they’re registered investment accounts, similar to an RRSP, that allows Canadians to invest up to a certain amount each year and generate tax-free returns.

Don’t pass up free money from the government, and that’s basically what a TFSA is, free money. If you’re generating investment returns outside of a registered investment account you’ll be required to pay taxes on it, so why pay taxes if you don’t have too?

With all that said, just like your RRSP, there is a limit to how much you can contribute to your TFSA.

I will leave a video here below on How to Check Your TFSA limit.

So please guys, don’t just use an RRSP for your retirement savings, because once you withdraw that money the tax man will come looking for their cut. But not with a TFSA.

In the quest to retire early as a Canadian, it’s so important to take full advantage of all your tax friendly investments accounts.

7. Increase Your Monthly Savings Rate

Have you ever considered bumping up your savings rate a few percentage points in order to retire a little earlier?

Canadians aren’t great savers. In fact, in 2018, the average net savings for Canadian households was $852 (Stats Canada).

So be the exception, be that one weird friend who saves way more than anyone else.

Try and increase your savings rate from 10%-25%. Or go even more drastic, try and save 40% of your income.

While that might not seem possible for a lot of people, and I get that, but believe it or not, it’s not as hard as it seems.

I actually started doing this last year, I watched a Grant Cardone Youtube video where he was talking about how you should save 40% of your income and it really motivated me.

So I redid my budget, cut back on my lifestyle, and started living off 60% of my pre-tax income.

Yes, at first it was hard, but I knew it was possible, the numbers were there, I just had to live a little more modestly.

After a while, it became normal and I can honestly say that my happiness level has not decreased one bit.

In fact, it may have increased knowing that I’ll now be able to retire 10 years earlier.

You know what else increasing your savings rate does? It motivates you to try and earn more money.

Related Financial Geek Article: What Percentage of Your Income Should You Invest | By Salary Range

8. Don’t Spend Money You Get Unexpectedly

At some point in your life, you’ll receive money unexpectedly.

Whether it be from a tax return, a big bonus at work or a large inheritance from a loved one, it happens.

What do most Canadians do? They spend it right away, in fact, they usually have their mind made up on what they’re going to spend it on before the money even hits their account.

Like Stanley from the Office when Michael lies to them and tells them they’re all getting bonuses, “honey go ahead and buy those drapes”.

My suggestion? Pretend you didn’t even get the money and throw it all towards your retirement fund.

Not very much fun I know.

Depending on how much you get, you can always take a small percentage of it and treat yourself, but if you’re serious about retiring early, put a large percentage of this money away and save it for retirement.

Due to compound interest, doing this over a 15-20 year period could legitimately help you retire 5-10 years earlier.

Were those Gucci shoes really worth 5-10 more years of work?

9. Plan to “Work” While Retired

Another great way to plan for retirement is to decide to work as a retiree.

Now you might think that statement makes no sense, and I guess it kind of doesn’t, but hear me out.

Just because you retire from your career at a certain age doesn’t mean you can’t work a job.

Retirees often find jobs that they have a specific interest in. While doing it for the money may play a small role in their decision to work in retirement, the main reason they do it is for self satisfaction and enjoyment.

For example, if you’re into sports, maybe you could work as an usher at the pro sporting arena in your local city or town.

Maybe you have a passion for tourism and you become a tour guide in the summer?

These types of jobs won’t make you rich, but they’ll put some extra money in your pocket which will reduce the amount of money you’ll need before you retire from your 9-5.

It’s important to note that planning to work a hobby-job in retirement is a great idea, you’ll still want to save up for retirement.

In other words, don’t rely on a retirement job for your retirement fund.

10. Automate Your Savings

We already know that Canadians aren’t typically great savers, but why?

One reason being is that we tell ourselves we’ll save what’s left over each month, but as we know, there is nothing ever left over. We’ll spend every last penny of what’s in our bank account.

So if you want to retire early as a Canadian, or any nationality for that matter, you really need to set up an automated savings plan.

In other words, have your investment account automatically take money out of your bank account every month.

Every investment platform (Currently using Wealthsimple) I’ve ever used has had auto-deposit functionality. Trust me, these platforms want all your money, so they make the deposit process very easy.

Set your withdrawal day for the same day you get paid, that way the money will hopefully be in and out of your account by the time you wake up in the morning.

Quick tip #1- It’s like you never even had it! How can you miss something you never had!

Jokes aside, automating your savings plan is a great way to stick to your plan of retiring early, it’s a simplified process that allows you not to have to think about putting money away each month.

Your hands are off the wheel, you can only spend what you have now, the rest is put away for retirement whether you like it or not.

11. Avoid Debt Completely

Canadians love debt for some reason, I don’t get it.

As of December 2020, Canadians owed on average $1.71 for every dollar of disposable income they earned. This is crazy.

Now I don’t want to sound too much like Dave Ramsey here, but I truly do agree with him when he talks about basically living a debt free life.

He believes that besides your mortgage, you should become completely debt free even before you start investing.

While I don’t completely agree with that, as paying off student loans can take years, I do agree that people who regularly carry consumer debt are hindering their ability to retire early.

So to start, cut up your credit cards.

I use a Visa debit. It acts the same as a Visa (so I can still online shop) but all my transactions come out of my debit account. It’s perfect.

And no, credit card reward points won’t help you retire early.

I mentioned it before but I’ll say it again, car payments are just so unnecessary, buy a used, reliable car and pay for it in cash. There are more than enough used car dealerships in Canada for you to find something to drive.

Your house is different, your house is a real asset, and while I still think you should pay it off as quickly as possible, it’s almost impossible in your early years not to have a mortgage unless you don’t own a house (or you’re super rich).

My friends make fun of me all the time for not using credit cards and for having an old, used car despite being able to afford a new one, I just don’t care. My goal is to retire early, not to drive fancy cars I can’t afford.

12. Have an Emergency Fund

Having an emergency fund of 3-6 months worth of expenses could really help you reach your early retirement goals.

How might you ask? How would having cash sitting around in a savings account help me reach my goal?

And it’s a good question, but it’s actually not really about the money here, it’s more about the security and insurance.

Remember earlier we talked about setting financial goals and then sticking to a plan, well having a fully funded emergency fund will help you stick to this plan.

For example, what if your car breaks down? Or the hot water boiler in your house craps out? Maybe a costly medical or dental bill?

These are all unavoidable parts of life that could cost you thousands of dollars, so you need to be prepared for them.

If you don’t have an emergency fund for situations like this, you’ll end up having to go into debt to pay for them, and as we know, debt and early retirement rarely go hand and hand.

Once you go into debt you’ll need to start paying off that debt with your income and your nicely crafted budget is now out the window. Next thing you know, you’ve thrown the budget out completely and you’re back living paycheck to paycheck and never end up retiring!

Okay, got a little carried away there, but you get my point. Having an emergency fund helps you avoid going into debt for unexpected circumstances and will help you stick to your budget.

For more information on emergency funds and how much you should have saved, check out my Emergency Fund Amount | How Much Should I Have Saved? Article.

13. Increase Your Annual Income

Increasing your annual income is another way to help you speed up your retirement goals as a Canadian.

We often think that avoiding $3 coffees and buying $7 lunches is the pathway to early retirement, or my favorite – only keeping a half tank of gas or less in your car at all times, that way your vehicle is lighter and better on gas.

And while yes, no doubt all of these things will help you speed up your retirement process, but consider the other side of the coin too, what if you increase your annual income?

Think about it, let’s say you ask for a $10,000 pay raise and you get it, you could buy a $10 meal at Tim Hortons every day and still have an additional $6,350/year to save for retirement (not including taxes here).

Forbes writes a great article here on how to go about asking for a pay raise.

So yeah, it may be a little awkward, money talk usually is, but what do you have to lose? They either say no, and you carry on with your life, or they say yes and you drastically speed up your retirement plans.

14. Downsize Your Home

In David Chilton’s famous personal finance book The Wealthy Barber, he talks about how Canadians often say they’ll downsize their retirement, but they rarely do.

So if you love your home and plan to live there forever, you can probably skip this tip, but if you’re not opposed to downsizing in retirement then this option could certainly help you shave off a few of your working years.

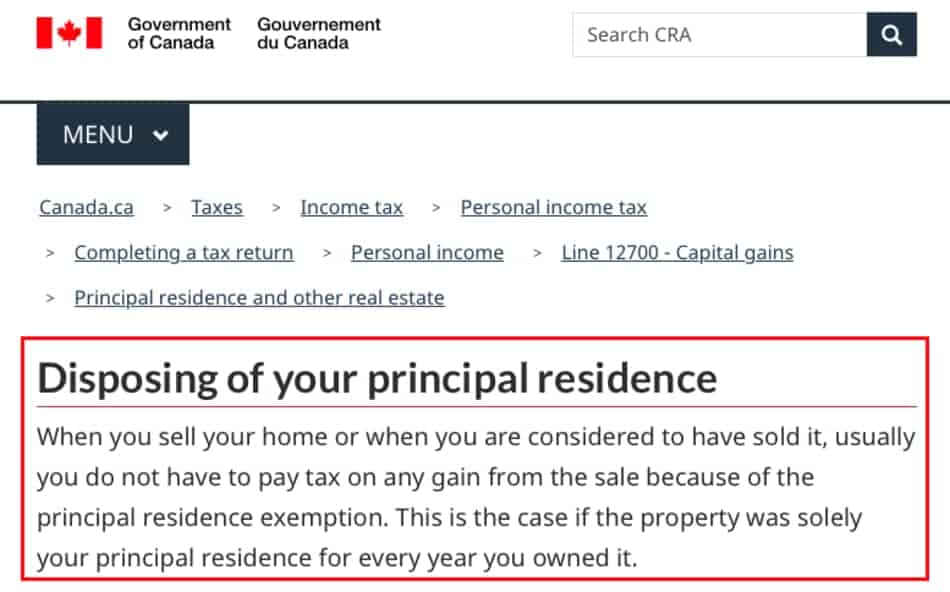

Let’s say you buy a house for $300,000 and you have it completely paid off. You then get it appraised and find out you’re able to sell it for $500,000. Well on paper, you’ve made $200,000 in capital gains on your home.

In order to realize your capital gain, you’ll need to sell your house, but with $500,000, you could buy another house that’s worth say…$250,000 and net out the other $250,000 and use it for retirement.

Not only that, but in Canada, you don’t have to pay taxes on any gains you make on your house as long as it’s your principal residence.

Now I’m giving you guys a pretty simplistic example here above, I’m assuming your home is paid off and the value of your home has increased in value by $200,000 – so again this probably isn’t your situation but that’s okay.

The point is, downsizing your home as a Canadian resident could really help expedite your retirement goals.

Disclaimer: While selling your house can help speed up your retirement process, I definitely wouldn’t rely on your home as a retirement fund as it’s impossible to know for sure what the housing market will look like then.

15. Live a Modest Lifestyle

Last but not least, en-route to an early retirement, try and live a very modest lifestyle.

Not only will living a modest lifestyle help you save more during your working years, but it will reduce the amount of money you’ll need in retirement.

I live in Canada, I have my whole life, the amount of people I know who live outside their means is shocking.

Instead of paying off debt, they buy brand new cars.

They say they can’t afford to invest but they buy designer brands.

$5,000 bonus? Gone. On what? They already forgot.

We always want new things, but that’s a game we just won’t win. The hamster wheel of consumption is a dangerous wheel to be on.

That’s why I choose to stay off it.

Buy a home you can actually afford, not what the bank tells you can afford and avoid eating at fancy restaurants multiple times a month.

I’m not saying you have to rough it, you work hard, enjoy the fruits of your labour, but just live below your means.

You know what the funny thing is, everyone I know that lives a modest lifestyle (relative to their income) actually seem to be quite happier than those that don’t.

They might not have the latest and greatest new iPhone every year, but does that stuff really make us happy?

You see, they aren’t bogged down by the constant need to “keep up with the joneses” – as that too is a game you won’t win.

Not only that, but as they don’t spend money on stupid stuff, they are able to save and invest more money to retire earlier, which in return makes them happier in knowing they’re future is looking real sunny.

And if you’re Canadian, you know “sunny” isn’t something we are too familiar with.

Conclusion

And there you have it, 15 tips and tricks to help you retire early as a Canadian.

Life happens fast, so start working on a plan for early retirement today. Once you get the snowball rolling, your motivation to retire at a young age will only increase.

Not everything discussed above will be something you take action on, and that is perfectly fine.

But pick 4-5 of them and track your results.

Geek, out.